Friday forecasts #2

5 forecasts: the price of oil in December as our target forecast, conditioned separately on the status of the Strait of Hormuz and the result of the US Senate election.

This is the second post in our series showcasing forecasts directly from Mantic.

This week’s focus is conditional forecasting: how explicit scenario modelling can help explain Mantic’s view of the future.

1. The price of oil in December 2026

Brent jumped almost 10 percent to $84 after the strikes resumed, its highest settle since mid-June. With the crisis unresolved and the Strait of Hormuz only shortly opened, where does crude settle by year end?

I predict the average price of Brent crude in December 2026 will be $78.25, with a 50% chance of falling between $72.00 and $84.50.

Downside pressure is expected to intensify late in the year as markets anticipate a massive 4.6 million b/d supply surplus in 2027, alongside declining oil demand in China due to rapid electric vehicle adoption.

Significant upside risk persists from a potential return to hostilities in the Middle East, where previous disruptions in 2026 drove prices toward $120; current thin OECD inventories provide little protection against such shocks.

Record non-OPEC+ production from the U.S., Brazil, and Canada acts as a structural headwind, likely capping sustained rallies unless significant geopolitical transit blockades re-emerge.

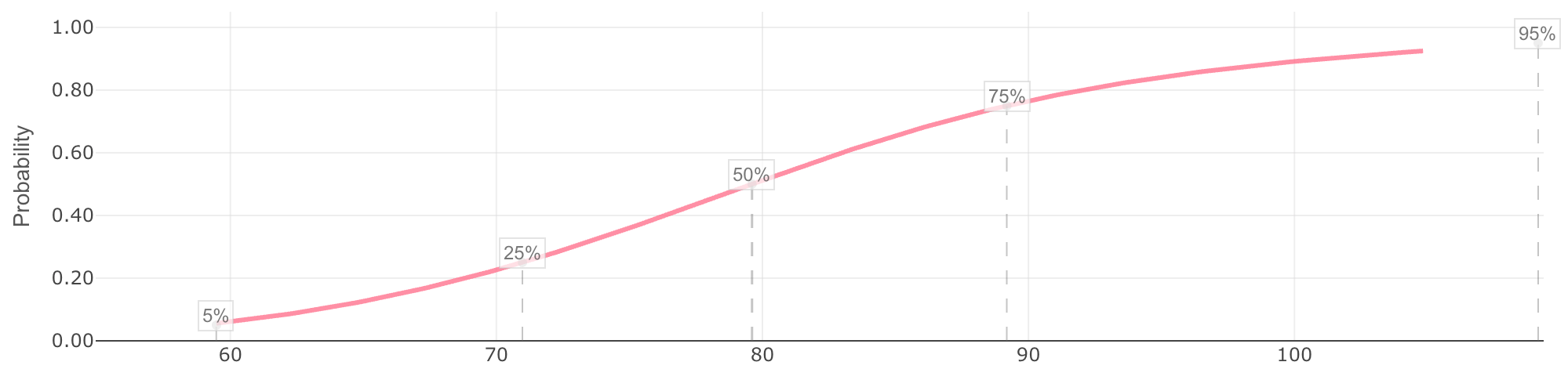

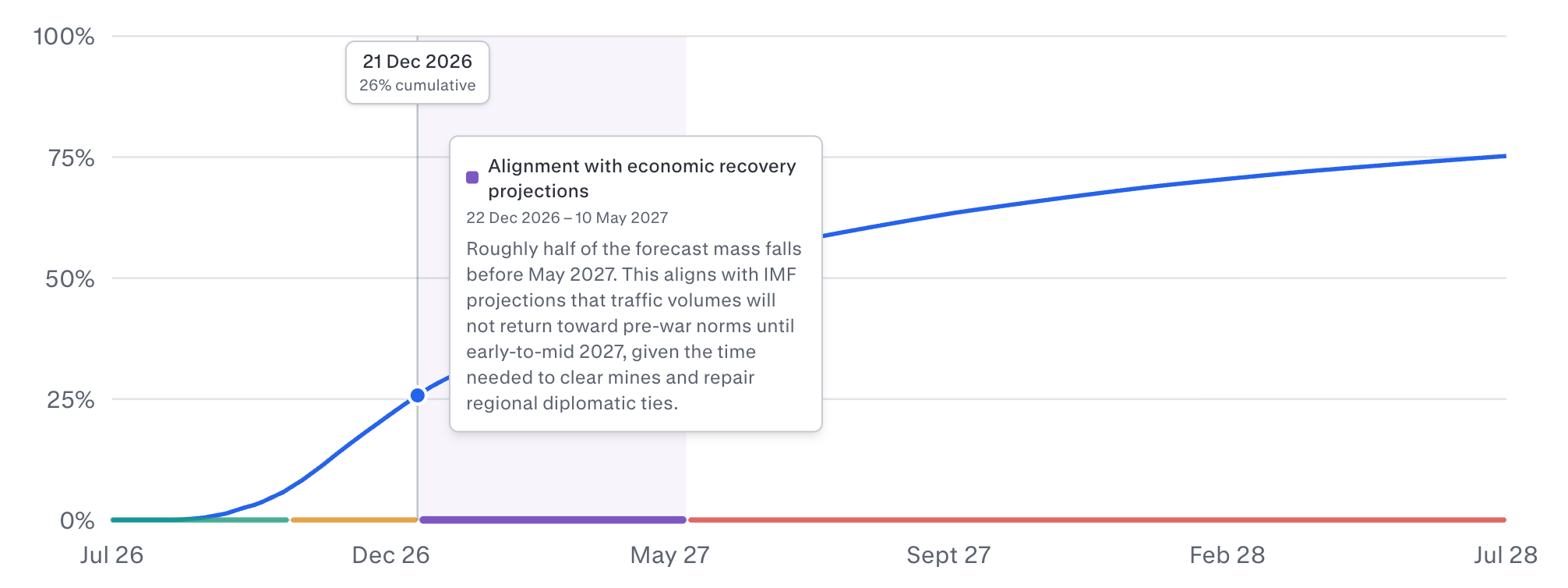

2. The Strait of Hormuz is open for at least 30 days before 2027

The Strait of Hormuz will be considered to have recovered if the 7-day moving average is at least 50 ships for 30 days straight, as in our previous post on the Iran conflict.

My median prediction for Strait of Hormuz transits recovering to a 7-day moving average of 50 for 30 consecutive days is 7th May 2027.

Current transit volumes have collapsed to 14-24 vessels per day following the July 14 reinstatement of a U.S. naval blockade and the breakdown of the June ceasefire.

The 50-transit threshold represents only one-third of the pre-war baseline of 138 daily transits, yet this level was not achieved even during the peak of the recent Islamabad Memorandum.

Major commercial carriers require approximately 30-45 incident-free days before resuming operations, meaning a sustained recovery cannot begin until well after a durable security agreement is reached.

Prohibitive war-risk insurance premiums at 5% of vessel value act as a primary economic barrier that I expect will persist until a decisive military outcome or political settlement occurs in early 2027.

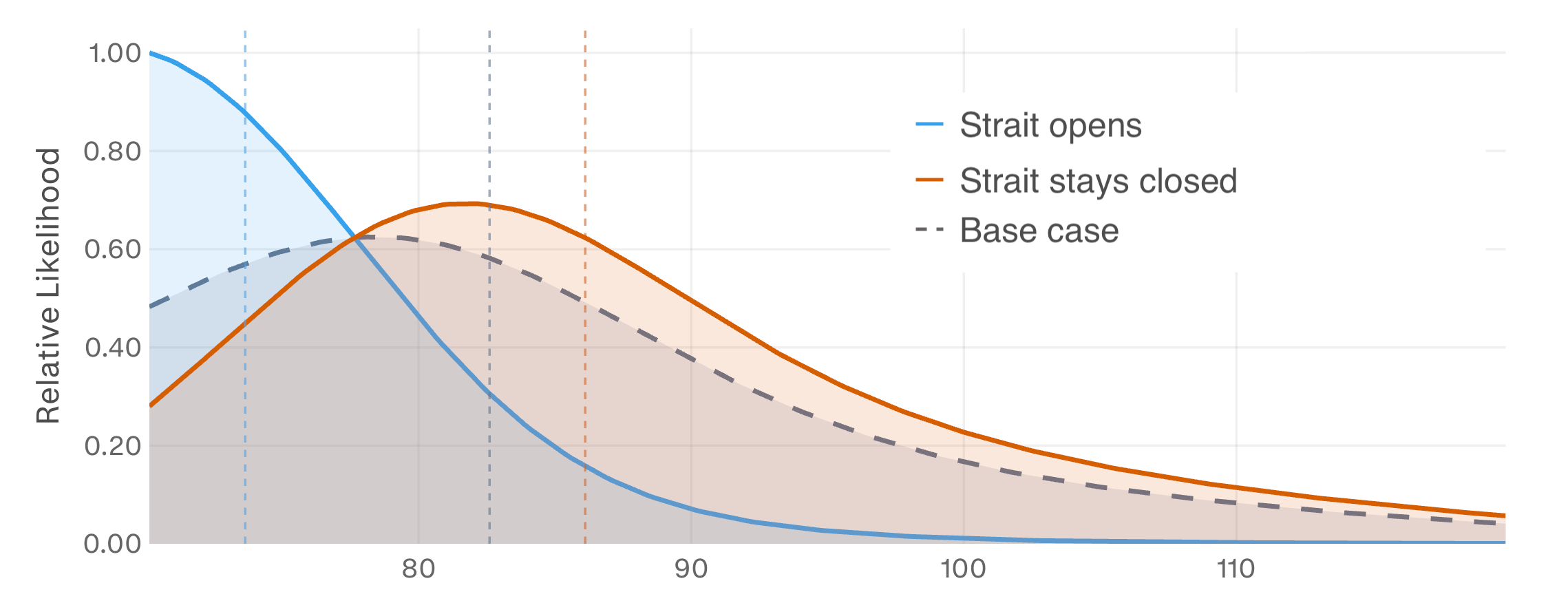

3. The price of oil in December 2026 conditional on the status of the Strait of Hormuz

As above, the Strait of Hormuz recovery is defined as the 7-day moving average being at least 50 ships for 30 straight days. Specifically for the conditional forecasts, the scenario is that this occurs before 2027, which Forecast 2 above showed being 28%.”

Strait of Hormuz recovery: YES

I primarily relied on the “futures curve”—the prices at which traders are currently agreeing to buy oil for delivery in late 2026. These market prices served as my strongest anchor, as they already reflect the collective wisdom of global participants. However, I adjusted these figures downward because the current market still prices in some possibility of continued disruption. By assuming the Strait is open, I accounted for a shift toward a market driven by supply and demand fundamentals rather than conflict.

On the fundamental side, I weighed reports from major energy agencies like the IEA and EIA, which suggest a transition toward a “looser” market by 2026. Factors such as increasing production from non-OPEC countries and a projected global oversupply heading into 2027 were key motivating factors. While I considered the possibility of sudden demand spikes or production cuts elsewhere, my thinking leaned toward a scenario where prices stabilize as the “fear factor” of shipping disruptions dissipates.

Strait of Hormuz recovery: NO

I first established a “business-as-usual” baseline using current futures markets and analyst consensus, which generally project prices in the $70–$85 range for late 2026. However, I determined that these estimates largely assume a return to geopolitical normalcy. By conditioning my forecast on the failure of transit levels to recover, I shifted my focus toward historical price spikes and risk scenarios modelled by international organisations like the World Bank.

My thinking balanced two competing forces. On the one hand, a persistent blockage or impairment of a major transit chokepoint suggests a significant “war risk premium” and potential supply shortages. On the other hand, I accounted for the global economy’s ability to adapt over several months. Factors such as the rerouting of oil through pipelines, increased production from non-OPEC countries, and potential demand destruction due to high prices would likely prevent an uncapped rally. Consequently, I favoured a distribution that sits notably higher than current market prices but remains grounded by long-term economic headwinds.

4. The democrats win control of the Senate

While far more uncertain than the House, a once unlikely control of the Senate by the Democrats has become a real possibility in the last year.

I predict the Republican Party will control the U.S. Senate after the 2026 elections with a 55% probability.

Structural advantages provide a critical buffer for the GOP, as the current 53-47 split and Vice President J.D. Vance’s tie-breaking vote allow Republicans to lose up to three net seats while maintaining the majority.

Democrats face a high bar for control, requiring a net gain of four seats to reach a 51-seat majority, a feat achieved by the opposition party in only 25% of cycles since 1980.

Significant headwinds including 4.2% inflation, low consumer sentiment, and underwater presidential approval ratings favour Democratic gains, particularly as Republicans must defend 22 of the 35 seats at stake.

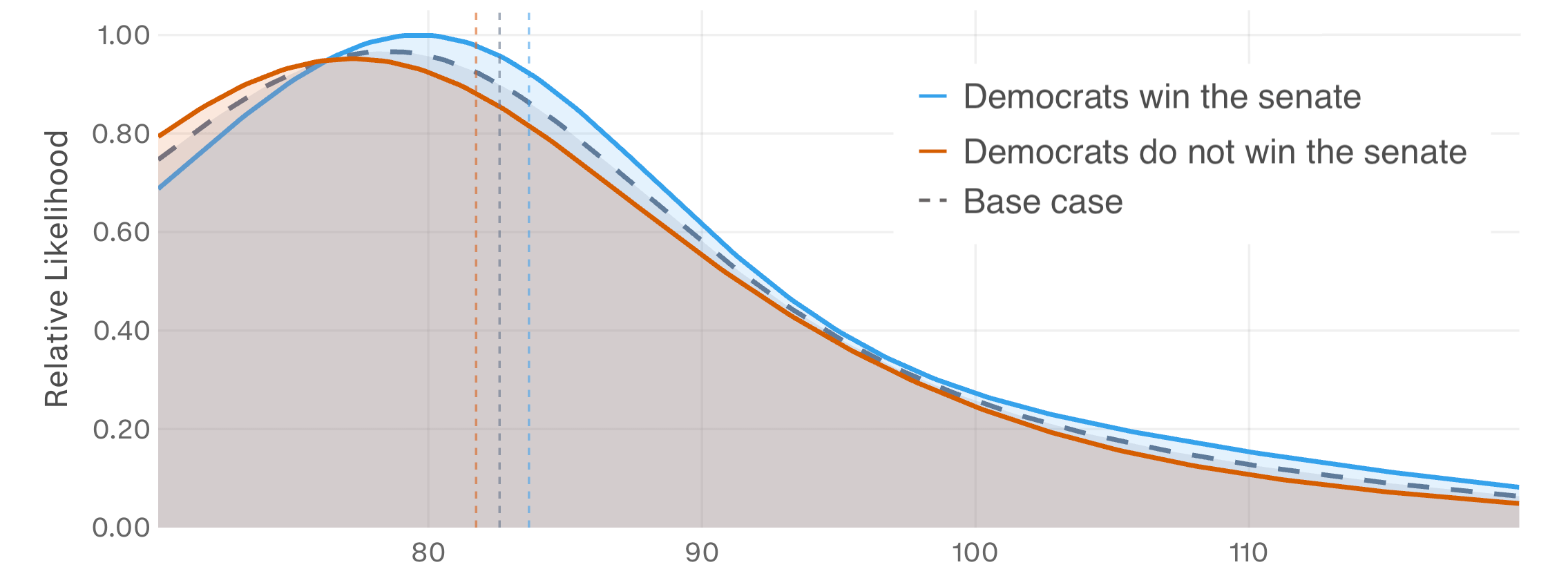

5. The price of oil in December 2026 conditional on the party in control of the Senate

Not all conditions move a price by acting on it directly. While the new Senate would only seat in early 2027, the results of the election will be known in November. Would the market react if Democrats took control of the Senate?

Democrats control of the Senate: YES

The specific condition of a Democratic Senate victory was factored in as a modestly “bullish” (price-supporting) element. I reasoned that a Democratic-controlled Senate would likely maintain tighter environmental regulations and be less aggressive in expanding domestic drilling permits compared to the alternative, slightly constraining future supply. However, because Brent is a globally traded commodity and the new Senate wouldn’t take office until after the forecast month, I treated this as a minor upward nudge rather than a transformative driver. Finally, I accounted for oil’s inherent volatility by maintaining wide “tails” in my distribution to cover the possibility of unexpected economic shocks or major supply disruptions.

Democrats control of the Senate: NO

Regarding the specific condition that the Democratic Party does not win the Senate, I viewed this as a “status quo” or slightly bearish factor. I reasoned that this outcome might favour domestic U.S. energy production and reduce the likelihood of new regulatory constraints, though I concluded the immediate impact on global oil prices within the same month as the election would be relatively modest. Finally, I maintained wide bounds to account for the high historical volatility of the oil market.